You’ll think you need a PhD in paperwork to figure HBCU aid—like it’s a secret ritual with stamps and smoke—and then you’ll breathe out, because it’s mostly forms, conversations, and a little strategy; I’ll show you how to pull the threads together. Picture us at the kitchen table, FAFSA open, scholarship emails buzzing, and you asking the exact questions that make financial aid officers sit up straight—short, targeted, no-nonsense. Want to know which grants stack, which don’t, and how work-study actually affects your monthly budget? Keep going.

Key Takeaways

- File the FAFSA early and meet state and campus deadlines to maximize federal, state, and institutional aid eligibility.

- Read award letters carefully to compare net cost, noting federal/state aid is applied before institutional scholarships.

- Ask the financial aid office whether scholarships stack, adjust, or replace other awards and confirm renewal requirements.

- Explore work-study, emergency funds, fee waivers, and departmental or alumni scholarships to reduce out-of-pocket costs.

- Create a family budget for tuition, housing, and unexpected expenses, and keep open communication with the aid office about changes.

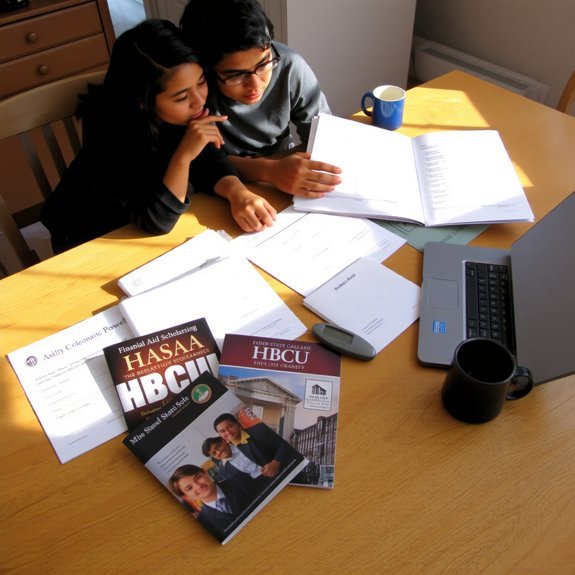

What Types of Financial Aid HBCUS Typically Offer

Money talk first: don’t let it scare you — you’ve got options. I’ll walk you through the usual aid menu so you can breathe, nod, and strategize. You’ll see grants that don’t need repayment, like institutional awards and sometimes merit grants, warm as free coffee on move-in day. Loans sit nearby — federal ones mostly, predictable and with income-based plans; private loans can taste bitter, so beware. Work-study lets your student earn cash, hands-on, campus lights humming as they clock hours. Scholarships pop up from the school, alumni, and departments; they sparkle, but you’ll have to apply or charm someone at the desk. Finally, fee waivers and emergency funds can rescue a surprise bill. You’re covered in layers.

How Federal and State Aid Work With Institutional Scholarships

If you’re juggling FAFSA forms and scholarship emails, don’t panic — I’ve got your back. You’ll find federal and state aid usually apply first, like the opening act, then institutional scholarships fill quieter gaps. Read award letters aloud, compare net costs, and don’t glaze over tiny footnotes — they bite. Picture stacking clear plastic trays: Pell Grant, state grant, then the school’s merit or need-based scholarship. Sometimes the college reduces its award if federal or state money increases, so ask whether their scholarships “stack” or “adjust.” Call the financial aid office, say, “Help me understand this,” and take notes. Keep receipts, timelines, polite persistence. You’ll negotiate smarter when you know which dollars are guaranteed, and which can shift.

Strategies to Maximize Grants and Work-Study Opportunities

Because you start with the FAFSA and keep nudging, you’ll stretch grant money farther than most parents realize — and yes, I say that from hard-earned experience and a drawer full of campus parking permits. I tell you the quick wins: file early, check deadlines, and update changes fast. Call the aid office, not just email — hear the person breathe, ask for specifics, write what they say. Split summer expenses with work-study earnings, pick jobs near classes so you smell cafeteria fries between shifts. Hunt outside grants — church groups, local businesses, even alumni clubs — and treat applications like mini essays, neat margins, clear goals. Track awards in a spreadsheet, celebrate small wins, and keep nudging; persistence pays.

Key Questions to Ask HBCU Financial Aid Offices

Wondering what to ask when you call the HBCU financial aid office — and yes, you should call — start with questions that get real answers, not scripted niceties. Ask: what’s my estimated aid package, and can you walk me through each line, slowly, like I’m learning guitar? Ask about deadlines that bite, emergency funds, and whether academic or cultural scholarships exist, the ones that don’t show up online. Ask who signs off on special circumstances, and request that person’s email, so you can stalk them politely. Ask how renewals work, what GPA triggers cuts, and whether summer credits count. Ask for timelines — when I’ll actually see money — and what documentation speeds things up. Keep a pen, breathe, and take notes; you’ll thank me.

Creating a Realistic Family Budget and Next Steps

When you sit down at the kitchen table, coffee steaming, laptop humming, and a stack of tuition forms threatening to avalanche, I want you to breathe and act like a budget detective — patient, curious, and a little stubborn. Start by listing fixed costs — mortgage, car, phone — then school bills, books, and that mystery fee nobody warned you about. Track two months of spending, yes with receipts, yes it’s tedious, you’ll thank me. Set a realistic monthly college line item, gently trim eating-out, subscriptions, impulse buys. Plan for emergencies, aim for a small savings buffer, and consider payment plans or work-study options. Finally, schedule a follow-up family meeting, update the plan, and celebrate small wins with dessert.

Conclusion

You’ve got this — picture the aid office like a lighthouse, its glow showing grants, loans, and work-study paths. Walk in, ask the blunt questions I’d ask if I were standing beside you, and read that award letter like a detective. Talk money at the kitchen table, budget like you mean it, and file FAFSA early. You’ll trim surprises, stretch scholarships, and watch your student’s future feel less like fog and more like daylight.

Leave a Reply